How Interest Rates Can Impact Your Monthly Housing Payments

Brent Wells March 3, 2020

Brent Wells March 3, 2020

Spring is right around the corner, so flowers are starting to bloom, and many potential homebuyers are getting ready to step into the market. If you’re thinking of buying this season, here’s how mortgage interest rates are working in your favor.

Freddie Mac explains:

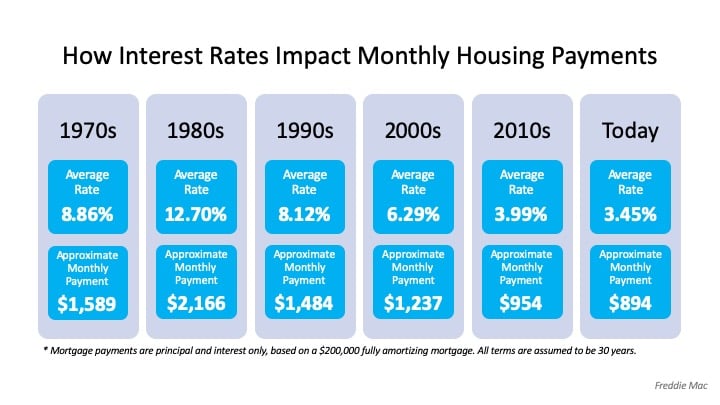

“If you’re in the market to buy a home, today’s average mortgage rates are something to celebrate compared to almost any year since 1971.

Mortgage rates change frequently. Over the last 45 years, they have ranged from a high of 18.63% (1981) to a low of 3.31% (2012). While it’s not likely that the average 30-year fixed mortgage rate will return to its record low, the current average rate of 3.45% is pretty close — all to your advantage.”

To put this in perspective, the following chart from the same article shows how average mortgage rates by decade have impacted the approximate monthly payment of a $200,000 home over time:

Clearly, when rates are low – like they are today – qualified buyers can benefit significantly over time.

Keep in mind, if interest rates go up, this can push many potential homebuyers out of the market. The National Association of Home Builders (NAHB) notes:

“Prospective home buyers are also adversely affected when interest rates rise. NAHB’s priced-out estimates show that, depending on the starting rate, a quarter-point increase in the rate of 3.75% on a 30-year fixed rate mortgage can price over 1.3 million U.S. households out of the market for the median-priced new home.”

You certainly don’t want to be priced out of the market this year, and waiting may mean a significant change in your potential mortgage payment should rates start to rise. If your financial situation allows, now may be a great time to lock in at a low mortgage rate to benefit greatly over the lifetime of your loan.

Stay up to date on the latest real estate trends.

If you're not already familiar with the Celina story, the numbers speak for themselves.

EV-Ready Living. Light Farms offers electric car charging stations within the community.

Buying a new construction home is a fundamentally different process than buying a resale property.

You’re clearing multiple rooms, a garage, attic, shed, or light remodel debris.

You find yourself only using part of the house while the rest collects dust.

Keeping the same flooring throughout the main living areas helps create a smooth, cohesive flow.

Overpricing, even by a little, can cause a listing to sit stale — which often leads to price drops.

Every week I am visiting with many new homes sales associates and I am hearing a consistent story.

North Sky is a June 2025 favorite, with new contemporary homes featuring open layouts and smart tech.

We'd love to hear from you! Whether you're buying, selling, or just exploring your options, we're here to provide answers, insights, and the support you need. Contact us and start planning your next move.