Bubble Alert - Is it Getting Too Easy to Get a Mortgage?

Brent Wells November 27, 2017

Brent Wells November 27, 2017

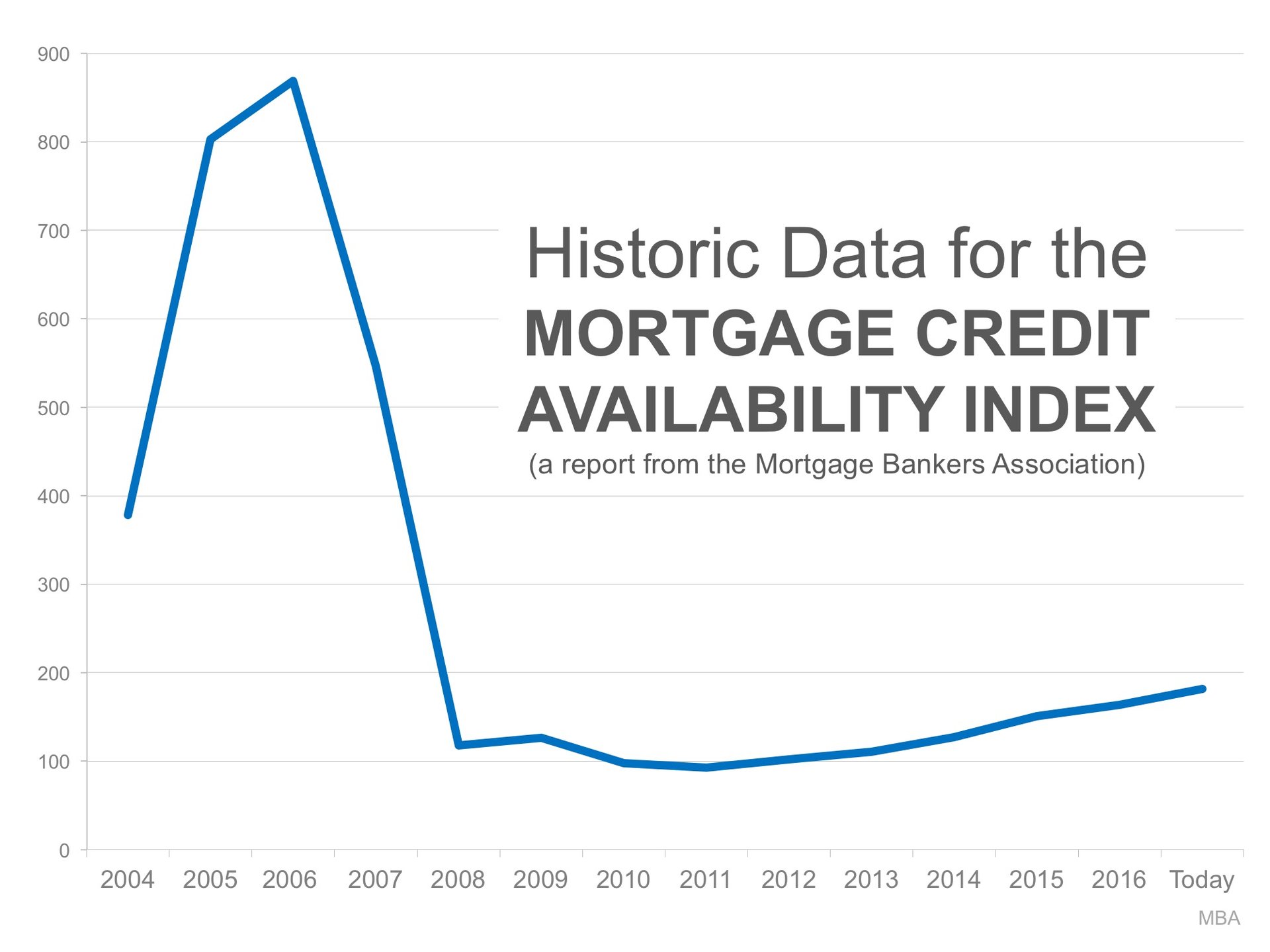

There is little doubt that it is easier to get a home mortgage today than it was last year. The Mortgage Credit Availability Index (MCAI), published by the Mortgage Bankers Association, shows that mortgage credit has become more available in each of the last several years. In fact, in just the last year:

This has some people worrying that we are returning to the lax lending standards which led to the boom and bust that real estate experienced ten years ago. Let’s alleviate some of that concern.

The graph below shows the MCAI going back to the boom years of 2004-2005. The higher the graph line, the easier it was to get a mortgage.

As you can see, lending standards were much more lenient from 2004 to 2007. Though it has gradually become easier to get a mortgage since 2011, we are nowhere near the lenient standards during the boom.

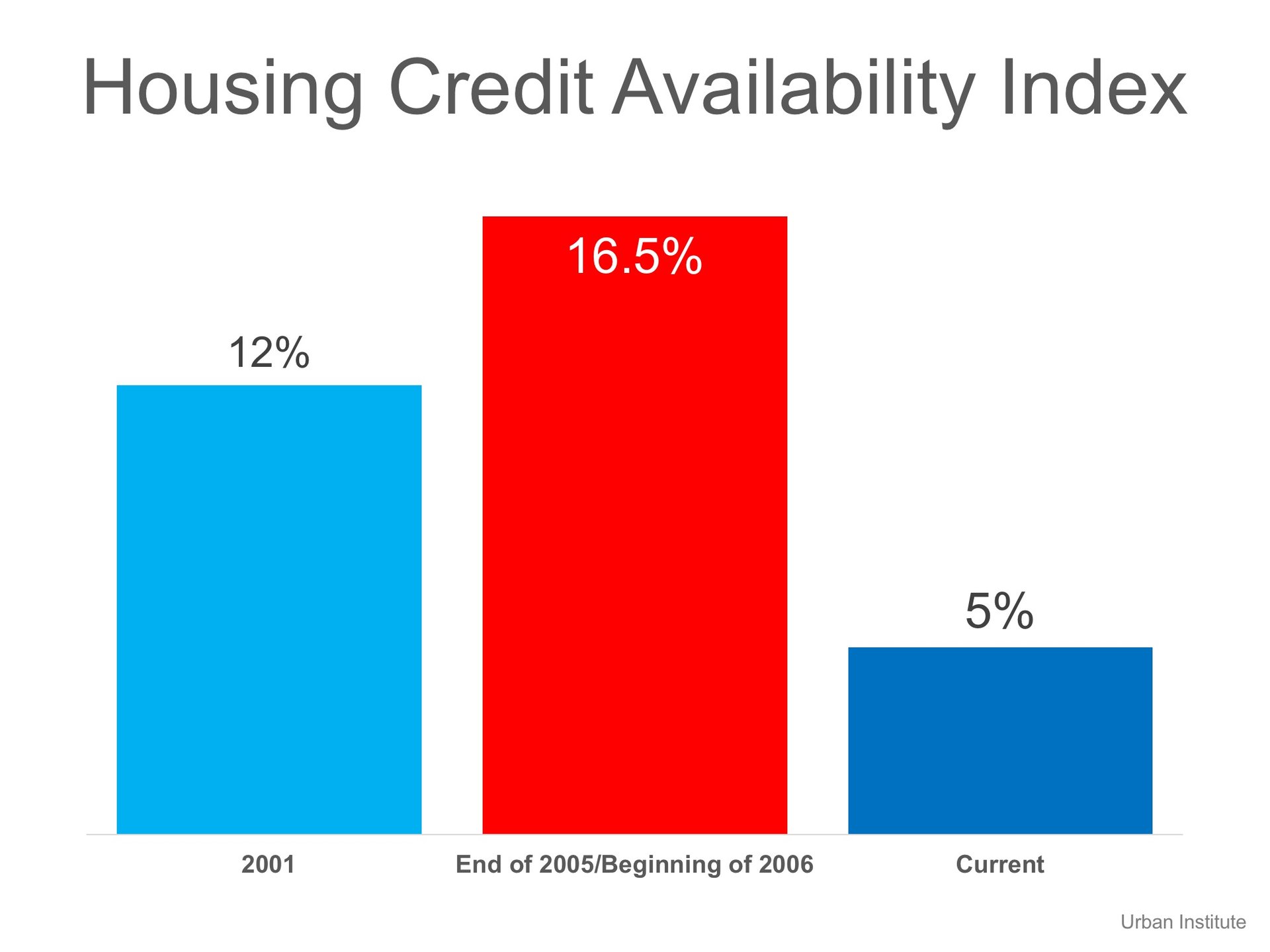

The Urban Institute also publishes a Home Credit Availability Index (HCAI). According to the Institute, the HCAI:

“Measures the percentage of home purchase loans that are likely to default—that is, go unpaid for more than 90 days past their due date. A lower HCAI indicates that lenders are unwilling to tolerate defaults and are imposing tighter lending standards, making it harder to get a loan. A higher HCAI indicates that it is easier to get a loan.”

Here is a graph showing their findings:

Again, today’s lending standards are nowhere near the levels of the boom years. As a matter of fact, they are more stringent than they were even before the boom.

It is getting easier to gain financing for a home purchase. However, we are not seeing the irresponsible lending that caused the housing crisis.

Stay up to date on the latest real estate trends.

If you're not already familiar with the Celina story, the numbers speak for themselves.

EV-Ready Living. Light Farms offers electric car charging stations within the community.

Buying a new construction home is a fundamentally different process than buying a resale property.

You’re clearing multiple rooms, a garage, attic, shed, or light remodel debris.

You find yourself only using part of the house while the rest collects dust.

Keeping the same flooring throughout the main living areas helps create a smooth, cohesive flow.

Overpricing, even by a little, can cause a listing to sit stale — which often leads to price drops.

Every week I am visiting with many new homes sales associates and I am hearing a consistent story.

North Sky is a June 2025 favorite, with new contemporary homes featuring open layouts and smart tech.

We'd love to hear from you! Whether you're buying, selling, or just exploring your options, we're here to provide answers, insights, and the support you need. Contact us and start planning your next move.